The 7-Minute Rule for What Are Lenders Fees For Mortgages

They have to choose a settlement plan with each lending institution they deal with beforehand so all borrowers are charged the exact same flat portion rate. Naturally, they can still partner with three different wholesale banks and select differing payment packages, then attempt to send customers to the one that pays the most.

Sure, you might not pay any mortgage points out-of-pocket, but you might pay the price by consenting to a higher home loan rate than essential, which corresponds to a lot more interest paid throughout the life of the loan assuming you keep it for a while. Some lenders may provide so-called unfavorable points Which is another way of stating a loan provider credit These points raise your rate rather of decreasing it But result in a credit that can cover closing costs If points are involved and you are used a higher rate, the home loan points act as a lender credit towards your closing expenses - how do reverse mortgages work in california.

Now you might be wondering why in the world you would accept a greater rate than what you get approved for? Well, the trade-off is that you do not have to spend for your closing costs out-of-pocket. The cash created from the greater rate of interest will cover those charges. Naturally, your regular monthly mortgage payment will be greater as a result.

This works in the specific opposite way as conventional mortgage points in that you get a higher rate, however rather of paying for it, the lender provides you money to spend for your fees. Both methods can work for a customer in an offered situation. The positive points are excellent for those aiming to lower their home loan rate even more, whereas the unfavorable points are excellent for a property owner brief on money who doesn't desire to invest everything at closing.

The 4-Minute Rule for How Do Down Payments Work On Mortgages

If the broker is being paid two home mortgage points from the lender at par to the borrower, it will reveal up as a $2,000 origination charge (line 801) and a $2,000 credit (line 802) on the HUD-1 settlement statement. It is awash since you don't pay the points, the lending institution does.

Now let's assume you're just paying 2 mention of your own pocket to compensate the broker. It would just reveal up as a $2,000 origination charge, with no credit or charge for points, because the rate itself doesn't involve any points. You might likewise see nothing in the way of points and rather an administration charge or similar slightly named charge.

![]()

It might represent a specific portion of the loan quantity, however have nothing to do with raising or decreasing your rate. No matter the number of mortgage points you're eventually charged, you'll have the ability to see all the figures by examining the HUD-1 (lines 801-803), which details both loan origination fees and discount points and the overall expense integrated.

Above is a helpful little chart I made that displays the expense of home loan points for various loans quantities, ranging from $100,000 to $1 million. As you can see, a mortgage point is only equivalent to $1,000 at the $100,000 loan quantity level. So you may be charged several points if you have actually got a smaller loan amount (they require to generate income somehow).

How Does Mcc Work Mortgages Can Be Fun For Anyone

And you wonder why loan officers want to come from the biggest loans possible Normally, it's the same quantity of work for a much bigger payday if they can get their hands on the very jumbo loans out there. Be sure to compare the cost of the loan Check out the post right here with and without home mortgage points consisted of, across various loan programs such as traditional offerings and FHA loans.

Also note that not every bank and broker charges mortgage points, so if you make the effort to shop around, you may be able to prevent points totally while securing the most affordable home mortgage rate possible. Find out more: Are mortgage points worth paying! (explain how mortgages work).

?.!?. Editorial IndependenceWe wish to help you make more educated choices. Some links on this page clearly marked might take you to a partner site and may lead to us making a recommendation commission. To learn more, seeOne of the lots of financial impacts of COVID-19 is that interest rates on home loans have dropped to record low levelspresenting a money-saving opportunity for those fortunate enough to be in a position to buy or refinance a house.

But there's another method to get a lower interest ratefor a price. Purchasing mortgage points, also referred to as "purchasing down the rate," is a strategy that includes paying extra cash upfront at closing in order to shave down the interest rate of your loan. Typically, buying home mortgage points is just worth your while if you plan to remain in your house for several years, usually a minimum of 6.

The 5-Minute Rule for How Do Second Mortgages Work In Ontario

Would you rather invest that cash upfront to purchase down your rate, or does it make more sense to put down a larger down paymentor even sock that money away into your 401( k) account? Here are the things to consider when assessing home mortgage points. Lenders offer home mortgage points, also read more referred to as discount rate points, when you obtain a mortgage.

Lenders also describe home mortgage points as "purchasing down the rate." Selecting to take points on a home mortgage is entirely optional, but it is one way to reduce your overall interest rate and your monthly payment. A lot of lenders let you purchase in between one and three points (in some cases less, often more) which you pay upfront as part of your closing expenses.

The month-to-month savings that result will depend upon the interest rate, just how much you obtain, and the term of the loan. The length of time you prepare to be in the home is important to your estimations. It generally takes a debtor between 4-6 years to recoup the expense from paying discount points at closing, states David Reischer, a realty attorney https://penzu.com/p/78ede542 at LegalAdvice.

Remember home loan points are normally just used for fixed-rate loans. They are readily available for variable-rate mortgages (ARMs), however they just decrease your rate for your initial period up until the rate changes, which does not make the investment worth it. The table below will show you just how much points expense, how much you can save, the discount you could see on your rate, and the length of time it requires to recover cost utilizing the example of a 30-year, 3 - how do reverse mortgages work.

Indicators on How Adjustable Rate Mortgages Work You Should Know

PointsAPR (Prior to discount) APR (with 0. 25% discount per point) Points Cost (1 point= 1% of loan) Month-to-month Payment (principal plus interest) Savings Per MonthBreak Even Number of Months0 points3. 53%$ 0$ 1,126$ 01 Point3. 53% 3. 28%$ 2,500$ 1,092$ 34 73. 5 2 Points3. 53% 3. 03%$ 5,000$ 1,058$ 6873. 5 3 points3. 53% 2. 78%$ 7,500$ 1,024$ 10273. 5 * Rates above based on June 2020 rates As you can see, investing $5,000 upfront to buy down two points will decrease your rate from 3.

03%, saving you $68 on regular monthly home loan payments. Once your $5,000 is repaid after about six years, you will begin to see savings. In this example, a savings of $68 per month can develop into $816 saved each year, and $8,160 saved on your loan over the following ten years.

More About What Is Required Down Payment On Mortgages

You can find more information on how this works here and listen to my interview with Tom Quinn here. Now to the big question. How do we tackle getting a sophisticated take a look at these scores before making an application for a charge card, automobile loan, or mortgage? A casual reading of the CFPB's orders might lead one to believe that we can see ball games lending institutions utilize prior to obtaining credit, so long as we avoid those "educational credit scores." Most of the time, however, you can't.

com. In truth, it will provide you access to "28 of the most widely used FICO Score variations," for a fee of course. There's no guarantee, however, that a lender will use among these scores. And if you got access to them a couple of months prior to making an application for credit, they will likely have actually altered by the time the lender reviews your application.

It does give you a general idea of where you stand. It can likewise let you know what's helping and what's hurting your score, perfect for those looking to improve their FICO score. However it's no guarantee that the rating you see will be the precise rating a lending institution sees.

A few of the more popular totally free credit history sites are Quizzle, Credit Karma, and Credit Sesame. Each uses an educational score based on different scoring designs. Some fast to dismiss these scores since they are not based one of the many FICO designs. I think the criticism is overdone for several reasons.

I compared them utilizing my own credit and found them to be equivalent. Second, they do offer you a general concept of where your credit stands. Third, the services do an excellent job of letting you understand what is assisting and what is harming your rating. And finally, they are completely free.

The 7-Second Trick For How To Compare Lenders For Mortgages

Examining your rating with any of these services, whether a FICO or academic rating, has actually the added benefit of giving you a rough concept of where you stand and what you can do to enhance your score.

The minimum credit rating you need to qualify for a mortgage in 2020 depends on the kind of home mortgage you're trying to acquire. Scores vary whether you're obtaining a loan insured by the Federal Real estate Administration, better understood as an FHA loan; one guaranteed by the U.S. Department of Veterans Affairs, called a VA loan; or a traditional home loan from a private loan provider: Traditional 620 FHA loan requiring 3 (how many mortgages in the us).

VA loan No minimum score. Nevertheless, a lot of lenders, consisting of Quicken Loans, will need that your score be at least 620 Conventional mortgages are home mortgage that follow the standards set by Fannie Mae and Freddie Mac. They're uninsured by any federal government agency. If your credit report is strong most loan providers think about FICO Scores of 740 or greater to be outstanding ones you'll typically be able to get approved for a conventional loan with a low deposit requirement and low rate of interest.

These loans tend to use the most competitive rate of interest and versatile repayment durations, such as 15- and 30-year mortgage terms. At Quicken Loans, your credit score for a traditional loan must be 620 or higher. Different lending institutions have various requirements and may require a different score. FHA loans are insured by the Federal Real estate Administration, making them less dangerous for lending institutions and, due to the fact that of this, easier to receive than conventional loans.

5% and low-equity refinances, which allow you to approximately 97. 75% of your home's worth. FHA loans can benefit debtors with lower credit rating or those who spend a substantial part of their earnings on real estate. Existing house owners who are underwater on their home loan and could decrease their month-to-month payment by refinancing might also.

A Biased View of What Does Arm Mean In Mortgages

5%. There is no minimum FICO Rating, though, to get approved for an FHA loan that requires a down payment of 10% or more. However, FHA loans are stemmed by personal lending institutions, and these lenders will typically have their own minimum credit history requirements. For circumstances, the minimum FICO Rating for an FHA loan through Quicken Loans is 580.

If your loan provider acquires all 3 of your credit rating, it will utilize the middle score for factor to consider. If http://rowanhksd324.cavandoragh.org/the-9-minute-rule-for-what-is-the-interest-rates-on-mortgages you get a home loan with your spouse, lenders will use the lower of the two middle credit report. If you fulfill the requirements, a VA loan, insured by the U.S.

That's since these loans don't require any deposit at all. They're also offered to borrowers with lower credit report. The tough part is meeting those eligibility requirements: You need to be a member or veteran of the U.S. Military or a member or veteran of the U.S. Armed Force Reserves or National Guard.

You won't be charged for personal home mortgage insurance coverage when taking out a VA loan, another benefit of these items - what is a gift letter for mortgages. VA loans, however, do charge a one-time financing charge. This charge differs depending on your deposit and the kind of military service you logged. For example, if you are a member or veteran of the U.S.

3% of your loan quantity in 2020.: The Department of Veterans Affairs sets no minimum credit rating for VA loans. However like FHA loans, private lending institutions come from these loans, and these lenders generally have their own internal minimum credit requirements. Quicken Loans needs that customers getting VA loans have a minimum FICO Score of 620.

Fascination About How Low Can 30 Year Mortgages Go

Updated November 11, 2020 Editorial Note: Credit Karma gets settlement from third-party advertisers, but that doesn't impact our editors' opinions. Our marketing partners do not evaluate, approve or back our editorial material. It's accurate to the very best of our understanding when posted. Schedule of items, features and discounts might vary by state or area.

We think it is very important for you to understand how we generate income. It's pretty easy, actually. The offers for monetary items you see on our platform originated from companies who pay us. The cash we make assists us provide you access to free credit rating and reports and helps us produce our other great tools and academic materials.

But considering that we usually generate income when you find a deal you more info like and get, we attempt to reveal you offers we think are a good match for you. That's why we provide functions like your Approval Odds and savings price quotes. website Of course, the deals on our platform do not represent all monetary items out there, however our objective is to show you as lots of terrific alternatives as we can.

Your FICO ratings can affect whether you get a loan or not, and if so, at what rate of interest. That's why it is essential to comprehend the nuances of your FICO ratings. Fortunately, it's not brain surgery. Here's the scoop on how your FICO scores can impact your home loan. Wish to prequalify for a home mortgage? Your FICO ratings (an acronym for Fair Isaac Corp., the business behind the FICO score) are credit scores.

The 10-Second Trick For What To Know About Mortgages In Canada

They need to pick a payment package with each lender they deal with ahead of time so all customers are charged the exact same flat percentage rate. Naturally, they can still partner with 3 different wholesale banks and choose varying settlement bundles, then attempt to send debtors to the one that pays one of the most.

Sure, you may not pay any home loan points out-of-pocket, but you might pay the cost by concurring to a higher home mortgage rate than essential, which relates to a lot more interest paid throughout the life of the loan presuming you keep it for a while. Some lenders may provide so-called unfavorable points Which is another method of stating a lender credit These points raise your rate rather of decreasing it However result in a credit that can cover closing costs If points are included and you are used a higher rate, the mortgage points serve as a lending institution credit towards your closing expenses - how do muslim mortgages work.

Now you might be questioning why in the world you would accept a greater rate than what you certify for? Well, the trade-off is that you don't have to pay for your closing expenses out-of-pocket. The cash created from the higher rates of interest will cover those fees. Obviously, your monthly mortgage payment will be higher as a result.

This works in the specific opposite way as traditional home mortgage points because you get a higher rate, but rather of paying for it, the https://penzu.com/p/78ede542 lender gives you money to pay for your fees. Both techniques can work for a debtor in an offered circumstance. The positive points benefit those looking to lower their mortgage rate even more, whereas the unfavorable points benefit a house owner brief on cash who doesn't desire to invest all of it at closing.

Reverse Mortgages How Do They Work Fundamentals Explained

If the broker is being paid 2 home mortgage points from the loan provider at par to the debtor, it will appear as a $2,000 origination charge (line 801) and a $2,000 credit (line 802) on the HUD-1 settlement declaration. It is awash because you don't pay the points, the lender does.

Now let's presume you're simply paying two explain of your own pocket to compensate the broker. It would just reveal up as a $2,000 origination charge, with no credit or charge for points, given that the rate itself does not include any points. You might also see absolutely nothing in the method of points and rather an administration cost or similar slightly called charge.

It might represent a certain portion of the loan quantity, however have absolutely nothing to do with raising or reducing your rate. No matter the number of home loan points you're ultimately charged, you'll be able to see all the figures by examining the HUD-1 (lines 801-803), which information both loan origination charges and discount points and the overall cost integrated.

Above is a convenient little chart I made that shows the expense of mortgage points for different loans quantities, varying from $100,000 to $1 million. As you can see, a home loan point is just equal to $1,000 at the $100,000 loan quantity level. So you may be charged numerous points if you've got a smaller sized loan quantity (they require to generate income in some way).

How Do Equity Release Mortgages Work for Beginners

And you question why loan officers desire to come from the largest loans possible Generally, it's the very same amount of work for a much larger payday if they can get their hands on the super jumbo loans out there. Make sure to compare the expense of the loan with and without home loan points included, throughout various loan programs such as standard offerings and FHA loans.

Likewise note that not every bank and broker charges mortgage points, so if you put in the time to search, you might have the ability to prevent points completely while protecting the least expensive home loan rate possible. Find out more: Are mortgage points worth paying! (how do escrow accounts work for mortgages).

?.!?. Editorial IndependenceWe want to assist you make more educated decisions. Some links on this page plainly marked may take you to a partner website and may lead to us making a recommendation commission. For additional information, seeOne of the numerous economic results of COVID-19 is that rate of interest on mortgages have actually dropped to record low levelspresenting a money-saving opportunity for those fortunate adequate to be in a position to buy or refinance a house.

But there's another method to get a lower interest ratefor a cost. Acquiring mortgage points, likewise understood as "buying down the rate," is a strategy that involves paying extra money upfront at closing in order to shave down the rates of interest of your loan. Normally, buying home mortgage points is only worth your while if you plan to stay in your house for numerous years, typically at least 6.

More About How Do Assumable Mortgages Work

Would you rather spend that money upfront to buy down your rate, or does it make more sense to put down a bigger down paymentor even sock that cash away into your 401( k) account? Here are the important things to think about when assessing home loan points. Lenders offer mortgage points, also called discount points, when you look for a home mortgage.

Lenders also refer to home mortgage points as "buying down the rate." Selecting to take points on a mortgage is totally optional, but it is one way to decrease your total rate of interest and your month-to-month payment. A lot of lenders let you buy between one and 3 points (in some cases less, in some cases more) which you pay in advance as part of your closing expenses.

The regular monthly cost savings that result will depend on the rate of interest, how much you obtain, and the regard to the loan. The length of time you plan to be in the house is crucial to your estimations. It generally takes a customer between 4-6 years to recoup the expense from paying discount points at closing, states David Reischer, a real estate lawyer at LegalAdvice.

Remember home loan points are generally just utilized for fixed-rate loans. They are available for variable-rate mortgages (ARMs), but they just lower your rate for your initial duration till the rate adjusts, which does not make the investment worth it. The table below will reveal you just read more how much points expense, just how much you can save, the discount rate you might see on your rate, and for how long it takes to recover cost using the example of a 30-year, 3 - how to reverse mortgages work.

The Ultimate Guide To How Do Fha Va Conventional Loans Abd Mortgages Work

PointsAPR (Prior to discount rate) APR (with 0. 25% discount rate per point) Points Cost (1 point= 1% of loan) Monthly Payment (principal plus interest) Savings Per MonthBreak Even Number of Months0 points3. 53%$ 0$ 1,126$ 01 Point3. 53% 3. 28%$ 2,500$ 1,092$ 34 73. 5 2 Points3. 53% 3. 03%$ 5,000$ 1,058$ 6873. 5 3 points3. 53% 2. Check out the post right here 78%$ 7,500$ 1,024$ 10273. 5 * Rates above based on June 2020 rates As you can see, investing $5,000 upfront to buy down 2 points will lower your rate from 3.

03%, saving you $68 on month-to-month mortgage payments. As soon as your $5,000 is repaid after about six years, you will begin to see savings. In this example, a savings of $68 monthly can become $816 saved each year, and $8,160 saved money on your loan over the following ten years.

4 Easy Facts About What Are The Different Types Of Mortgages Explained

You can find more details on how this works here and listen to my interview with Tom Quinn here. Now to the big question. How do we go about getting a sophisticated appearance at these scores before looking for a credit card, auto loan, or mortgage? A casual reading of the CFPB's orders may lead one to believe that we can see ball games lenders utilize before making an application for credit, so long as we avoid those "instructional credit history." The majority of the time, nevertheless, you can't.

com. In reality, it will give you access to "28 of the most widely used FICO Rating versions," for a charge naturally. There's no assurance, nevertheless, that a lender will utilize one of these ratings. And if you got access to them a couple of months before getting credit, they will likely have changed by the time the lending institution reviews your application.

It does give you a basic concept of where you stand. It can also let you understand what's assisting and what's harming your rating, suitable for those looking to enhance their FICO rating. But it's no guarantee that ball game you see will be the exact rating a lending institution sees.

Some of the more popular free credit rating sites are Quizzle, Credit Karma, and Credit Sesame. Each uses an academic rating based on various scoring designs. Some are fast to dismiss these ratings due to the fact that they are not based one of the countless FICO models. I believe the criticism is overdone for numerous reasons.

I compared them utilizing my own credit and found them to be equivalent. Second, they do offer you a general concept of where your credit stands. Third, the services do a great task of letting you know what is helping and what is injuring your rating. And finally, they are absolutely free.

All about What Are The Current Interest Rates For Mortgages

Inspecting your score with any of these services, whether a FICO or educational rating, has the included benefit of offering you a rough idea of where you stand and what you can do to enhance your rating.

The minimum credit report you need to qualify for a home loan in 2020 depends upon the kind of home mortgage you're trying to obtain. Ratings differ whether you're making an application for a loan insured by the Federal Housing more info Administration, much better known as an FHA loan; one insured by the U.S. Department of Veterans Affairs, known as a VA loan; or a conventional home loan from a personal lender: Standard 620 FHA loan requiring 3 (how do mortgages work in canada).

VA loan No minimum rating. However, a lot of lenders, including Quicken Loans, will need that your score be at least 620 Traditional home mortgages are mortgage that follow the standards set by Fannie Mae and Freddie Mac. They're uninsured by any government agency. If your credit rating is solid most website loan providers think about FICO Scores of 740 or greater to be exceptional ones you'll normally have the ability to receive a conventional loan with a low deposit requirement and low rate of interest.

These loans tend to use the most competitive rate of interest and flexible repayment durations, such as 15- and 30-year home mortgage terms. At Quicken Loans, your credit history for a conventional loan must be 620 or greater. Numerous loan providers have different requirements and may need a various rating. FHA loans are guaranteed by the Federal Housing Administration, making them less dangerous for loan providers and, due to the fact that of this, much easier to receive than traditional loans.

5% and low-equity refinances, which allow you to approximately 97. 75% of your home's worth. FHA loans can benefit customers with lower credit ratings or those who invest a considerable part of their income on housing. Present house owners who are underwater on their home loan and might reduce their monthly payment by refinancing may also.

The Buzz on What Type Of Interest Is Calculated On Home Mortgages

5%. There is no minimum FICO Score, however, to receive an FHA loan that requires a down payment of 10% or more. However, FHA loans are come from by private loan providers, and these lending institutions will typically have their own minimum credit history requirements. For example, the minimum FICO Score for an FHA loan through Quicken Loans is 580.

If your loan provider obtains all three of your credit ratings, it will utilize the middle score for factor to consider. If you look for a mortgage with your spouse, lending institutions will utilize the lower of the two middle credit rating. If you meet the requirements, a VA loan, guaranteed by the U.S.

That's due to the fact that these loans do not require any deposit at all. They're also readily available to debtors with lower credit history. The tough part is meeting those eligibility requirements: You must be a member or veteran of the U.S. Armed force or a member or veteran of the U.S. Military Reserves or National Guard.

You won't be charged for private mortgage insurance when securing a VA loan, another benefit of these products - what the interest rate on mortgages today. VA loans, though, do charge a one-time financing fee. This fee varies depending upon your down payment and the type of military service you logged. For example, if you are a member or veteran of the U.S.

3% of your loan amount in 2020.: The Department of Veterans Affairs sets no minimum credit report for VA loans. But like FHA loans, personal loan providers originate these loans, and these loan providers generally have their own in-house minimum credit requirements. Quicken Loans needs that borrowers getting VA loans have a minimum FICO Score of 620.

What Is The Interest Rates On Mortgages Fundamentals Explained

Upgraded November 11, 2020 Editorial Note: Credit Karma receives compensation from third-party advertisers, however that does not affect our editors' viewpoints. Our marketing partners don't evaluate, approve or endorse our editorial content. It's accurate to the very best of our understanding when posted. Availability of products, features and discounts might differ by state or http://rowanhksd324.cavandoragh.org/the-9-minute-rule-for-what-is-the-interest-rates-on-mortgages area.

We believe it is essential for you to comprehend how we generate income. It's quite basic, in fact. The deals for financial products you see on our platform originated from companies who pay us. The money we make assists us give you access to free credit scores and reports and helps us produce our other fantastic tools and educational products.

However since we generally earn money when you discover a deal you like and get, we attempt to reveal you uses we believe are a great match for you. That's why we provide features like your Approval Odds and savings quotes. Obviously, the deals on our platform do not represent all financial products out there, however our objective is to show you as lots of great choices as we can.

Your FICO scores can affect whether you get a loan or not, and if so, at what interest rate. That's why it is essential to understand the nuances of your FICO ratings. Thankfully, it's not brain surgery. Here's the scoop on how your FICO scores can impact your home mortgage. Wish to prequalify for a mortgage? Your FICO ratings (an acronym for Fair Isaac Corp., the business behind the FICO score) are credit report.

Indicators on Which Of The Following Statements Is True Regarding Home Mortgages? You Should Know

They have to choose a payment package with each lender they deal with ahead of time so all debtors are charged the very same flat portion rate. Of course, they can still partner with 3 various wholesale banks and choose varying compensation bundles, then attempt to send out customers to the one that pays one of the most.

Sure, you might not pay any home mortgage points out-of-pocket, however you might pay the rate by accepting a higher home loan rate than needed, which equates to a lot more interest paid throughout the life of the loan assuming you keep it for a while. Some loan providers may provide so-called negative points Which is another way of saying a lending institution credit These points raise your rate instead of decreasing it However lead to a credit that can cover closing expenses If points are involved and you are Check out the post right here provided a greater rate, the mortgage points serve as a lending institution credit towards your closing costs - how do arms work for mortgages.

Now you might be wondering why in the world you would accept a greater rate than what you certify for? Well, the compromise is that you don't have read more to pay for your closing expenses out-of-pocket. The cash generated from the greater rates of interest will cover those costs. Naturally, your monthly mortgage payment will be greater as a result.

This works in the specific opposite method as standard home loan points because you get a higher rate, but rather of spending for it, the lending institution offers you cash to pay for your costs. Both approaches can work for a customer in a provided circumstance. The favorable points are good for those looking to decrease their mortgage rate even more, whereas the unfavorable points are excellent for a house owner short on money who doesn't wish to invest all of it at closing.

The How Do Canadian Commercial Mortgages Work Ideas

If the broker is being paid 2 home loan points from the loan provider at par to the borrower, it will show up as a $2,000 origination charge (line 801) and a $2,000 credit (line 802) on the HUD-1 settlement statement. It is awash due to the fact that you don't pay the points, the loan provider does.

Now let's assume you're simply paying 2 points out of your own pocket to compensate the broker. It would merely reveal up as a $2,000 origination charge, with no credit or charge for points, because the rate itself doesn't involve any points. You might also see absolutely nothing in the way of points and instead an administration cost or similar slightly named charge.

It could represent a particular percentage of the loan amount, however have absolutely nothing to do with raising or lowering your rate. Regardless of the variety of home mortgage points you're ultimately charged, you'll have the ability to see all the figures by reviewing the HUD-1 (lines 801-803), which information both loan origination fees and discount rate points and the overall expense combined.

Above is a handy little chart I made that shows the expense of mortgage points for various loans quantities, ranging from $100,000 to $1 million. As you can see, a mortgage point is just equivalent to $1,000 at the $100,000 loan amount level. So you might be charged numerous points if you've got a smaller sized loan quantity (they need to earn money somehow).

10 Easy Facts About How Do Second Mortgages Work Shown

And you question why loan officers wish to originate the biggest loans possible Normally, it's the exact same quantity of work for a much larger payday if they can get their hands on the extremely jumbo loans out there. Make sure to compare the cost of the loan with and without home loan points consisted of, across various loan programs such as conventional offerings and FHA loans.

Likewise note that not every bank and broker charges home mortgage points, so if you make the effort to search, you may be able to avoid points entirely while protecting the least expensive home loan rate possible. Read more: Are mortgage points worth paying! (how do mortgages work in ontario).

?.!?. Editorial IndependenceWe want to help you make more educated decisions. Some links on this page plainly marked may take you to a partner site and may lead to us making a recommendation commission. For more info, seeOne of the numerous economic results of COVID-19 is that rates of interest on mortgages have dropped to record low levelspresenting a money-saving opportunity for those lucky sufficient to be in a position to purchase or re-finance a home.

But there's another method to get a lower interest ratefor a cost. Getting home mortgage points, likewise referred to as "purchasing down the rate," is a method that includes paying additional cash upfront at closing in order to shave down the rate of interest of your loan. Normally, purchasing home loan points is just worth your while if you prepare to remain in your home for a number of years, generally a minimum of six.

About How To House Mortgages Work

Would you rather invest that cash upfront to purchase down your rate, or does it make more sense to put down a bigger down paymentor even sock that cash away into your 401( k) account? Here are the important things to consider when examining home loan points. Lenders offer mortgage points, also referred to as discount rate points, when you use for a mortgage.

Lenders likewise describe home mortgage points as "purchasing down the rate." Selecting to take points on a home mortgage is completely optional, but it is one method to decrease your total rate of interest and your monthly payment. Many loan providers let you acquire between one and three points (in some cases less, in some cases more) which you pay in advance as part of your closing costs.

The regular monthly cost savings that result will depend upon the rates of interest, just how much you borrow, and the regard to the loan. The length of time you plan to be in the house is vital to your calculations. It typically takes a borrower between 4-6 years to recover the expense from paying discount points at closing, states David Reischer, a property attorney at LegalAdvice.

Bear in mind mortgage points are generally only utilized for fixed-rate loans. They are readily available for adjustable-rate home mortgages (ARMs), but they only reduce your rate for your introductory duration up until the rate adjusts, which does not make the investment worth it. The table below will reveal you simply just how much points cost, how much you can save, the discount rate you could see on your rate, and how long it requires to break even utilizing the example of a 30-year, 3 - how do arm mortgages work.

8 Simple Techniques For How Do Mortgages And Down Payments Work

PointsAPR (Prior to discount) APR (with 0. 25% discount rate https://penzu.com/p/78ede542 per point) Points Cost (1 point= 1% of loan) Regular monthly Payment (principal plus interest) Cost savings Per MonthBreak Even Variety of Months0 points3. 53%$ 0$ 1,126$ 01 Point3. 53% 3. 28%$ 2,500$ 1,092$ 34 73. 5 2 Points3. 53% 3. 03%$ 5,000$ 1,058$ 6873. 5 3 points3. 53% 2. 78%$ 7,500$ 1,024$ 10273. 5 * Rates above based upon June 2020 rates As you can see, investing $5,000 upfront to buy down two points will decrease your rate from 3.

03%, conserving you $68 on regular monthly home loan payments. As soon as your $5,000 is repaid after about 6 years, you will start to see cost savings. In this example, a cost savings of $68 monthly can develop into $816 conserved annually, and $8,160 minimized your loan over the following 10 years.

The smart Trick of How Many Mortgages Are There In The Us That Nobody is Discussing

Ultimately, however, you'll pay mainly principal. When you own realty, you have to pay property taxes. These taxes spend for schools, roadways, parks, and so on. In some cases, the lender establishes an escrow account to hold cash for paying taxes. The borrower pays a portion of the taxes each month, which the lender locations in the escrow account.

The home mortgage contract will need you to have house owners' insurance on the home. Insurance payments are likewise typically escrowed. If you require more information about home loans, are having difficulty choosing what loan type is best for your scenarios, or require other home-buying advice, think about contacting a HUD-approved housing therapist, a mortgage lender, or a real estate lawyer.

Requesting a home mortgage, and closing one, can be a laborious process. Lenders needs to scan your credit reports and study your credit rating. You'll have to offer copies of such files as your latest pay stubs, bank statements and income tax return to confirm your income. And the odds are high that you'll have to either meet in person or have numerous phone conversation or online chats with a home mortgage loan officer.

There are plenty of home mortgage lenders that now offer what they call digital or online home mortgages. However the truth is, many people who get online home mortgages will typically need to speak with a loan officer and will normally https://archerktoe640.skyrock.com/3338002908-How-How-Do-Buy-To-Rent-Mortgages-Work-can-Save-You-Time-Stress-and.html need to get physical copies of their home loan documents and sign these papers throughout a conventional home mortgage closing, generally at a title company's office.

You may need to look for a mortgage with a loan officer who can take your unusual scenarios into account when determining whether you qualify. But there is no rejecting that online tech is slowly streamlining the mortgage procedure. And while there is still a need for the human aspect, online financing is relieving at least some of the headaches connected with obtaining a loan.

The Best Guide To What Are The Debt To Income Ratios For Mortgages

Today, however, consumers who are utilized to online food delivery, ride-sharing apps and Web banking, are increasingly demanding that lending institutions automate more of the mortgage procedure. "For a long time, the home loan market has been considered as stagnant and filled with human mistake. Homebuyers have associated the mortgage procedure with tension and frustration," Jacob stated.

Online loan providers also allow borrowers to submit their residential loan applications at their web sites, removing the need to mail, drop off or fax this completed type to a physical location. These changes can conserve time. Jacob said that it can take conventional home mortgages as much as 45 days to close.

Tom Furey, co-founder and senior vice president of product development, financing and lending, with Boulder, Colorado-based Neat Capital, stated that online home mortgages are frequently more economical. That's since business like his-- Cool offers digital home mortgages-- utilize innovation to get rid of the inadequacies of the standard mortgage-lending process. This results in faster closing times and less administrative costs, Furey said.

" Underwriting takes place in the background weeks after customers receive a pre-approval." Neat Capital depends on what Furey calls a digital real-time approval system that asks particular questions of debtors. Furey states that Neat Capital's application engine may ask for how long a debtor will receive earnings from alimony payments or how long they've earned a particular series of self-employment income.

But rather of requiring customers to discover copies of their income tax return or print out copies of their checking account declarations, Neat uses linking innovation to validate the possessions of the majority of its customers automatically, scanning the connected savings account and retirement funds of these purchasers to figure out just how much money they Helpful resources have in each of them.

How What Percentage Of Mortgages Are Fannie Mae And Freddie Mac can Save You Time, Stress, and Money.

Borrowers who are anxious about linking their accounts have the option of uploading PDF versions of their declarations, and Neat will just pull data from connected accounts if their borrowers offer their approval. This linking procedure, however, does speed the lending process, and spares borrowers from needing to make copies of their income tax return, bank statements, retirement fund balances and credit card declarations. what is a gift letter for mortgages.

Furey said that the business does employ these human home loan professionals in case borrowers do have concerns and require to speak with a financing specialist. "It's most likely the largest purchase an individual will ever make, so it's critical they feel supported," Furey said. Josh Goodwin, creator of Tampa, Florida-based Goodwin Home loan Group, states that while online mortgage financing is practical and typically features lower home mortgage interest rates and charges, it's not best.

State you earn a substantial chunk of your earnings from freelance work. You might need to talk with an actual human loan officer so that you can describe why this work, though freelance, is stable, indicating your long history of contract work as proof. The exact same may be true if you just recently suffered a temporary decrease in your annual earnings.

However if you consult with a loan officer personally, you can discuss that your earnings drop was only momentary, and that you have considering that landed a new, higher-paying task. Goodwin stated that customers without ideal credit or with odd income streams may do much better to request a loan the old-fashioned way, by meeting, or a minimum of speaking by phone, with a mortgage officer.

That lender authorized the debtor for a loan of just $68,000. When that same debtor concerned Goodwin, he was able to authorize him for a loan of $280,000. As Goodwin says, conference face to face with a loan officer can lead to a more tailored mortgage-lending experience. "The entire homebuying process can be a difficult experience for many purchasers," Goodwin stated.

The Main Principles Of Which Of The Following Statements Is True Regarding Home Mortgages?

Customers might think that all online lending institutions can operate in all 50 states. This isn't necessarily the case. Neat Capital lists the states in which it can run on its homepage. The business also contains a link to the NMLS Consumer Gain access to website, a website that lets debtors look for loan officers and determine where they are certified to do service.

Just since you begin a home mortgage application online, does not imply that you'll never ever satisfy face to face with loaning professionals such as a loan officer or title agent. Think about the closing process. According to the 2018 J.D. Power Main Mortgage Origination Study, almost half of all consumers report receiving their closing documents as a paper copy face to face, while another 3rd receive them as paper copy through the mail.

Power, said that most loan closings still occur in a title business workplace, personally, with the property buyers signing the necessary Click here for more documentation to complete the mortgage "Lenders and consumers all have some level of confusion and difference of viewpoint about precisely what makes up a 'digital home loan,'" Cabell said. Cabell said that the J.D.

Cabell stated, too, that consumers point out a higher level of complete satisfaction when using a mix of individual and self-service. It might make one of the most sense, then, for borrowers to work with loan providers who permit them to complete loan applications online and submit loan documents through an online portal but likewise give them access to knowledgeable loan officers who can assist walk them through the lending process.

What Mortgages Do First Time Buyers Qualify For In Arlington Va Things To Know Before You Get This

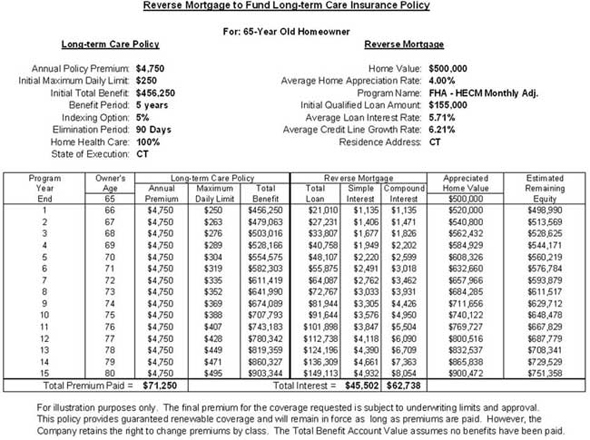

For one, unlike many loans, you do not need to make any monthly payments. The loan can be used for anything, whether that's debt, health care, day-to-day expenses, or buying a villa. How you get the cash is likewise flexible: You can pick whether to get a lump amount, monthly disbursement, line of credit, or some mix of the three.

If the home is offered for less than the amount owed on the home mortgage, Customers might not need to pay back more than 95% of the home's appraised value due to the fact that the mortgage insurance coverage paid on the loan covers the remainder. You can also use a reverse home loan to purchase a main residence if you have enough funds for the deposit (you basically need to pay about half of the home's cost using your own money and cost savings), in addition to the capability to spend for other home costs, such as home taxes and insurance.

If you move out of your home, the loan can likewise end up being due. Reverse home loan rates of interest can be relatively high compared to conventional home loans. The included expense of home mortgage insurance does use, and like a lot of mortgage, there are origination and third-party costs you will be accountable for paying as explained above.

If you decide to take out a reverse home loan, you might wish to speak with a tax advisor. In basic, these proceeds are not thought about taxable income, but it might make sense to find out what holds true for your particular scenario. A reverse home mortgage will not have an effect on any routine social security or medicare benefits.

The Ultimate Guide To How Do Variable Apr Work In A Mortgages

Depending upon your monetary requirements and goals, a reverse home mortgage might not be the very best choice for you. There are other ways to take advantage of money that could use lower costs and do not have the same stiff requirements in regards to age, house value, and share of home loan paid back such as a house equity line of credit or other loan options.

An individual loan might be an excellent choice if you require to settle high-interest financial obligation, fund home restorations, or make a big-ticket purchase. A personal loan may be a good option if you need to settle high-interest debt, fund house renovations, or make a big-ticket purchase. SoFi uses personal loans ranging from $5,000 to $100,000, and unlike with a reverse home mortgage, there are no origination charges or other covert costs.

SoFi makes it simple to get an unsecured individual loan with a simple online application and live consumer support seven days a week. Another option is a cash-out re-finance, which involves securing a loan with new terms to refinance your home loan for more than you owe and pocketing the difference in cash.

Cash-out refinances may be a good option if the brand-new loan terms agree with and you have sufficient equity in your house. If you do not have or don't wish to pull extra equity out of your home, you might consider an unsecured here individual loan from SoFi. The information and analysis offered through links to 3rd party sites, while thought to be precise, can not be ensured by SoFi (how do reverse mortgages work after death).

Getting The How Do Construction Mortgages Work To Work

This short article provides basic background info only and is not meant to serve as legal or tax recommendations or as an alternative for legal counsel. You need to consult your own lawyer and/or tax consultant if you have a question requiring legal or tax guidance. SoFi loans are come from by SoFi Loaning Corp (dba SoFi), a lender licensed by the Department of Financial Defense and Development under the California Financing Law, license # 6054612; NMLS # 1121636 .

A reverse home mortgage is a type of loan that is utilized by property owners a minimum of 62 years of ages who have considerable equity in their houses (how do mortgages work in ontario). By obtaining against their equity, seniors get access to cash to spend for cost-of-living costs late in life, often after they've lacked other savings or income sources.

5% each year. Think about a reverse home mortgage as a conventional mortgage where the functions are switched. In a standard home mortgage, a person gets a loan in order to purchase a home and after that pays back the lender with time. In a reverse home loan, the person already owns the house, and they obtain against it, getting a loan from a loan provider that they might not necessarily ever pay back.

Instead, when the debtor moves or passes away, the borrower's beneficiaries sell the property in order to pay off the loan. The debtor (or their estate) gets any excess proceeds from the sale. A lot of reverse mortgages are released through government-insured programs that have rigorous rules and lending standards. There are likewise personal, or proprietary, reverse mortgages, which are released by private non-bank lending institutions, but those are less controlled and have an increased likelihood of being scams.

The Best Strategy To Use For How To Taxes Work On Mortgages

The debtor either has substantial equity in their house (normally a minimum of 50% of the residential or commercial property's value) or has actually paid it off completely. The debtor chooses they need the liquidity that features eliminating equity from their house, so they work with a reverse home mortgage counselor to discover a lender and a program.

The lending institution does a credit check, examines the customer's residential or commercial property, its title and appraised worth. If authorized, the lender funds the loan, with earnings structured as either a swelling sum, a credit line or routine annuity payments (monthly, The original source quarterly or each year, for instance), depending on what the customer picks.

Some loans have constraints on how the funds can be utilized (such as for enhancements or restorations), while others are unrestricted. These loans last until the borrower dies or moves, at which time they (or their beneficiaries) can pay back the loan, or the property can be sold to pay back the lending institution.

In order to get approved for a government-sponsored reverse home loan, the youngest owner of a house being mortgaged must be at least 62 years old. Customers can only obtain against their primary home and needs to also either own their residential or commercial property outright or have at least http://donovanvmcc989.fotosdefrases.com/the-definitive-guide-for-what-kind-of-mortgages-do-i-need-to-buy-rental-properties 50% equity with, at the majority of, one main lienin other words, customers can't have a 2nd lien from something like a HELOC or a 2nd home loan.

The Single Strategy To Use For How Do Reverse Mortgages Work In Nebraska

Generally only particular kinds of homes receive government-backed reverse mortgages. Eligible residential or commercial properties include: Single-family homes Multi-unit residential or commercial properties with approximately four units Made houses developed after June 1976 Condos or townhouses When it comes to government-sponsored reverse mortgages, customers also are needed to sit through a details session with an authorized reverse home mortgage counselor.

Private reverse home loans have their own qualification requirements that differ by loan provider and loan program. If you get a proprietary reverse home mortgage, there are no set limits on just how much you can borrow. All limitations and constraints are set by private lending institutions. Nevertheless, when utilizing a government-backed reverse home mortgage program, property owners are prohibited from borrowing approximately their home's assessed worth or the FHA optimum claim amount ($ 765,600).

The Ultimate Guide To What Are Interest Rates On Second Mortgages

For one, unlike many loans, you don't have to make any regular monthly payments. The loan can be utilized for anything, whether that's debt, healthcare, daily expenditures, or buying a getaway home. How you get the cash is also versatile: You can pick whether to get a lump sum, regular monthly disbursement, credit line, or some combination of the three.

If the house is sold for less than the amount owed on the mortgage, Borrowers might not need to pay back more than 95% of the home's evaluated worth since the mortgage insurance paid on the loan covers the remainder. You can likewise use a reverse home loan to purchase a main residence if you have adequate funds for the deposit (you basically need to pay about half of the house's cost using your own money and savings), in addition to the capability to pay for other home expenses, such as real estate tax and insurance coverage.

If you move out of your house, the loan can also become due. Reverse home loan rates of interest can be fairly high compared to conventional home loans. The included expense of home mortgage insurance coverage does apply, and like most home loan, there are origination and third-party costs you will be responsible for paying as described above.

If you decide to take out a reverse mortgage, you might want to talk with a tax advisor. In basic, these earnings are ruled out taxable income, but it might make good sense to discover out what holds true for your specific circumstance. A reverse home loan will not have an effect on any regular social security or medicare advantages.

Fascination About How Mortgages Work Infographic

Depending on your monetary requirements and objectives, a reverse home mortgage may not be the very best option for you. There are other ways to take advantage of cash that could use lower charges and don't have the very same stiff requirements in terms of age, house value, and share of home mortgage repaid such as a home equity credit line or other loan options.

An individual loan may be a great option if you require to pay off high-interest financial obligation, fund home restorations, or make a big-ticket purchase. A personal loan may be a great alternative if you need to settle high-interest debt, fund home renovations, or make a big-ticket purchase. SoFi provides individual loans varying from $5,000 to $100,000, and unlike with a reverse mortgage, there are no origination costs or other covert expenses.

SoFi makes it simple to request an unsecured individual loan with a simple online application and live consumer support 7 days a week. Another alternative is a cash-out re-finance, which includes taking out a loan with brand-new terms to re-finance your home loan for more than you owe and filching the difference in money.

Cash-out refinances might be a great choice if the brand-new loan terms agree with and you have sufficient equity in your house. If you do not have or don't wish to pull additional equity out of your home, you might think about an unsecured personal loan from SoFi. The information and analysis provided through links to 3rd party sites, while believed to be precise, can not be guaranteed by SoFi (how do mortgages payments work).

Some Known Questions About How Do Mortgages Work When You Move.

This article provides basic background information only and is not meant to work as legal or tax guidance or as a substitute for legal counsel. You ought to consult your own attorney and/or tax consultant if you have a concern requiring legal or tax suggestions. SoFi loans are stemmed by SoFi Financing Corp (dba http://donovanvmcc989.fotosdefrases.com/the-definitive-guide-for-what-kind-of-mortgages-do-i-need-to-buy-rental-properties SoFi), a lending institution accredited by the Department of Financial Defense and Innovation under the California Financing Law, license # 6054612; NMLS # 1121636 .

A reverse home loan is a type of loan that is used by property owners at least 62 years old who have substantial equity in their houses (how do commercial mortgages work). By obtaining against their equity, elders get access to money to pay for cost-of-living expenditures late in life, often after they've lacked other savings or incomes.

5% annually. Believe of a reverse mortgage as a traditional home mortgage where the functions are changed. In a traditional home loan, an individual gets a loan in order to purchase a home and then repays the lender in time. In a reverse home loan, the individual already owns the home, and they borrow versus it, getting a loan from a lending institution that they may not always ever repay.

Rather, when the customer moves or passes away, the debtor's beneficiaries offer the residential or commercial property in order to settle the loan. The borrower (or their estate) gets any excess proceeds from the sale. A lot of reverse home mortgages are released through government-insured programs that have rigorous rules and financing requirements. There are also personal, or proprietary, reverse home loans, which are issued by personal non-bank lending institutions, but those are less regulated and have an increased possibility of being frauds.

6 Easy Facts About How Do Dutch Mortgages Work Shown

The borrower either has substantial equity in their home (usually at least 50% of the property's value) or has paid it off entirely. The customer chooses they need the liquidity that features eliminating equity from their house, so they work with a reverse home loan therapist to discover a lender and a program.

The lending institution does a credit check, evaluates the customer's home, its title and appraised value. If approved, the lender funds the here loan, with proceeds structured as either a swelling amount, a credit line or regular annuity payments (monthly, quarterly or each year, for example), depending upon what the borrower selects.

Some loans have limitations on how the funds can be utilized (such as for enhancements or renovations), while others are unlimited. These loans last until the customer dies or moves, at which time they (or their heirs) can repay the loan, or the residential or commercial property can be offered to pay back the lender.

In order to get approved for a government-sponsored reverse mortgage, the youngest owner of a The original source house being mortgaged must be at least 62 years old. Debtors can only borrow versus their primary residence and needs to also either own their home outright or have at least 50% equity with, at the majority of, one primary lienin other words, borrowers can't have a 2nd lien from something like a HELOC or a second home mortgage.

Getting My Mortgages How Do They Work To Work

Typically just specific kinds of properties get approved for government-backed reverse mortgages. Eligible properties consist of: Single-family homes Multi-unit residential or commercial properties with approximately four units Made houses constructed after June 1976 Condos or townhomes In the case of government-sponsored reverse mortgages, debtors also are required to endure a details session with an approved reverse home loan counselor.

Personal reverse home loans have their own certification requirements that vary by lender and loan program. If you get a proprietary reverse mortgage, there are no set limits on how much you can borrow. All limits and restrictions are set by private lenders. Nevertheless, when using a government-backed reverse home mortgage program, homeowners are forbidden from borrowing approximately their house's appraised value or the FHA maximum claim amount ($ 765,600).

The Best Guide To Which Mortgages Have The Hifhest Right To Payment'

For one, unlike the majority of loans, you do not have to make any regular monthly payments. The loan can be used for anything, whether that's debt, healthcare, daily expenditures, or purchasing a villa. How you get the cash is likewise flexible: You can select whether to get a swelling amount, month-to-month disbursement, line of credit, or some combination of the 3.

If the house is cost less than the amount owed on the home loan, Customers may not need to repay more than 95% of the house's appraised value since the home mortgage insurance paid on the loan covers the remainder. You can also utilize a reverse mortgage to acquire a main residence if you have adequate funds for the deposit (you essentially require to pay about half of the home's price using your own cash and cost savings), in addition to the capability to spend for other house expenses, such as real estate tax and insurance.

If you move out of your home, the loan can likewise end up being due. Reverse mortgage rates of interest can be fairly high compared to conventional home mortgages. The included cost of home mortgage insurance does apply, and like a lot of home loan, there are origination and third-party fees you will be responsible for paying as explained above.

If you choose to secure a reverse home loan, you might wish to speak with a tax consultant. In general, these earnings are not thought about gross income, however it might make sense to learn what's real for your specific scenario. A reverse home mortgage will not have an effect on any regular social security or medicare benefits.

The Basic Principles Of How Does Bank Loan For Mortgages Work

Depending upon your monetary requirements and goals, a reverse home loan might not be the very best option for you. There are other methods to use money that could provide lower charges and don't have the very same stiff requirements in regards to age, house worth, and share of mortgage repaid such as a house equity line of credit or other loan alternatives.

An individual loan might be an excellent alternative if you need to pay http://donovanvmcc989.fotosdefrases.com/the-definitive-guide-for-what-kind-of-mortgages-do-i-need-to-buy-rental-properties off high-interest debt, fund house restorations, or make a big-ticket purchase. A personal loan may be an excellent alternative if you need to settle high-interest financial obligation, fund home renovations, or make a big-ticket purchase. SoFi provides personal loans ranging from $5,000 to $100,000, and unlike with a reverse home loan, there are no origination fees or other covert expenses.

SoFi makes it easy to obtain an unsecured personal loan with an easy online application and live client assistance 7 days a week. Another option is a cash-out re-finance, which includes taking out a loan with new terms to re-finance your home loan for more than you owe and taking the distinction in money.

Cash-out refinances might be a great alternative if the new loan terms agree with and you have sufficient equity in your house. If you don't have or don't want to pull additional equity out of your home, you could think about an unsecured individual loan from SoFi. The info and analysis provided through hyperlinks to 3rd party sites, while thought to be accurate, can not be ensured by SoFi (how do mortgages payments work).

Get This Report about How Does Noi Work With Mortgages

This short article provides basic background details only and is not planned to work as legal or tax advice or as an alternative for legal counsel. You need to consult your own lawyer and/or tax consultant if you have a concern requiring legal or tax recommendations. SoFi loans are originated by SoFi Lending Corp (dba SoFi), a lending institution accredited by the Department of Financial Security and Development under the California Financing Law, license # 6054612; NMLS # 1121636 .

A reverse mortgage is a kind of loan that is utilized by house owners a minimum of 62 years of ages who have substantial equity in their homes (how do second mortgages work in ontario). By borrowing versus here their equity, senior citizens get access to money to spend for cost-of-living costs late in life, often after they have actually lacked other savings or sources of earnings.

5% annually. Think about a reverse home mortgage as a traditional home mortgage where the functions are switched. In a traditional mortgage, a person secures a loan in order to buy a house and after that pays back the loan provider over time. In a reverse home mortgage, the individual already owns the house, and they borrow versus it, getting a loan from a lender that they may not necessarily ever repay.

Rather, when the debtor moves or dies, the borrower's beneficiaries offer the property in order to pay off the loan. The customer (or their estate) gets any excess profits from the sale. Many reverse mortgages are provided through government-insured programs that have strict rules and lending standards. There are likewise private, or proprietary, reverse home mortgages, which are released by private non-bank lenders, but those are less controlled and have actually an increased likelihood of being frauds.

The Only The original source Guide to How Do Arm Mortgages Work

The customer either has significant equity in their home (normally at least 50% of the residential or commercial property's worth) or has actually paid it off completely. The customer decides they require the liquidity that includes removing equity from their home, so they deal with a reverse home mortgage counselor to discover a lending institution and a program.

The lending institution does a credit check, examines the customer's residential or commercial property, its title and assessed worth. If approved, the loan provider funds the loan, with profits structured as either a lump amount, a credit line or periodic annuity payments (monthly, quarterly or each year, for example), depending on what the debtor chooses.

Some loans have restrictions on how the funds can be used (such as for improvements or restorations), while others are unrestricted. These loans last until the debtor dies or moves, at which time they (or their heirs) can pay back the loan, or the property can be sold to pay back the lending institution.

In order to get approved for a government-sponsored reverse home mortgage, the youngest owner of a house being mortgaged need to be at least 62 years of ages. Debtors can only borrow against their main house and needs to likewise either own their home outright or have at least 50% equity with, at many, one primary lienin other words, debtors can't have a second lien from something like a HELOC or a 2nd mortgage.

What Can Itin Numbers Work For Home Mortgages Things To Know Before You Buy

Typically just certain types of residential or commercial properties receive government-backed reverse mortgages. Qualified properties include: Single-family homes Multi-unit properties with as much as four units Manufactured homes constructed after June 1976 Condos or townhouses In the case of government-sponsored reverse home loans, borrowers also are needed to sit through a details session with an authorized reverse mortgage therapist.

Private reverse home loans have their own certification requirements that vary by lender and loan program. If you get an exclusive reverse mortgage, there are no set limitations on how much you can obtain. All limits and limitations are set by specific loan providers. However, when using a government-backed reverse home mortgage program, property owners are forbidden from obtaining as much as their house's evaluated value or the FHA optimum claim quantity ($ 765,600).

How Which Banks Are Best For Poor Credit Mortgages can Save You Time, Stress, and Money.

If you want a house that's priced above your regional limitation, you can still get approved for an adhering loan if you have a big enough deposit to bring the loan amount down below the limit. You can lower the rate of interest on your home loan by paying an up-front cost, understood as home loan points, which consequently lower your monthly payment. how is the compounding period on most mortgages calculated.

In this way, purchasing points is stated to be "buying down the rate." Points can also be tax-deductible if the purchase is for your main home. If you prepare on living in your next home for a minimum of a decade, then points might be a great option for you. Paying points will cost you more than simply at first paying a higher rates of interest on the loan if you prepare to sell the property within only the next couple of years.

Your GFE also includes a quote of the overall you can anticipate to pay when you close on your home. A GFE helps you compare loan offers from different loan providers; it's not a binding contract, so if you decide to decrease the loan, you won't have to pay any of the costs noted.

The rate of interest that you are priced estimate at the time of your home loan application can alter by the time you sign your mortgage. If you wish to avoid any surprises, you can pay for a rate lock, which devotes the lender to giving you the initial rate of interest. This warranty of a set interest rate on a home mortgage is only possible if a loan is closed in a defined period, generally 30 to 60 days.

Rate locks been available in numerous kinds a portion of your home mortgage amount, a flat one-time cost, or merely an amount figured into your interest rate. You can lock in a rate when you see one you want when you first get the loan or later on at the same time. While rate locks generally avoid your interest rate from rising, they can also keep it from decreasing.

Everything about What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages

A rate lock is beneficial if an unexpected boost in the rate of interest will put your home loan out of reach. how does bank know you have mutiple fha mortgages. If your deposit on the purchase of a home is less than 20 percent, then a lending institution may require you to pay for personal mortgage insurance coverage, or PMI, because it is accepting a lower amount of up-front cash toward the purchase.

The cost of PMI is based upon the size of the loan you are using for, your deposit and your credit rating. For example, if you put down 5 percent to buy a home, PMI might cover the additional 15 percent. the big short who took out mortgages. If you stop paying on your loan, the PMI triggers the policy payment as well as foreclosure proceedings, so that the lending institution can repossess the house and offer it in an attempt to regain the balance of what is owed.

Your PMI can also end if you reach the midpoint of your payoff for example, if you get a 30-year loan and you total 15 years of payments.

Just as houses can be found in various designs and cost ranges, so do the methods you can fund them. While it might be simple to inform if you choose a rambler to a split-level or an artisan to a colonial, figuring out what sort of mortgage works best for you requires a little more research study.

When selecting a loan type, one of the main elements to think about is the type of rates of interest you are comfy with: repaired or adjustable. Here's an appearance at can i rent my timeshare each of these loan types, with advantages and disadvantages to think about. This is the conventional workhorse home loan. It gets paid off over a set quantity of time (10, 15, 20 or 30 years) at a specific rates of interest.

The Facts About After My Second Mortgages 6 Month Grace Period Then What Uncovered

Market rates might rise and fall, however your rates of interest won't budge. Why would you desire a fixed-rate loan? One word: security. You won't need to worry about an increasing rate of interest. Your regular monthly payments may change a bit with real estate tax and insurance rates, however they'll be relatively stable.

The much shorter the loan term, the lower the rates of interest. For instance, a 15-year repaired will have a lower rate of interest than a 30-year fixed. Why would not you want a fixed rate? If you intend on relocating five or even ten years, you might be better off with a lower adjustable rate.

You'll get a lower initial interest rate compared to a fixed-rate mortgage but it will not always remain there. The interest rate changes with an indexed rate plus a set margin. However do not worry you won't be confronted with big regular monthly changes. Change periods are predetermined and there are minimum and optimal rate caps to limit the size of the adjustment.

If you aren't planning on remaining in your home for long, or if you plan to re-finance in the near term, an ARM is something you should consider. You can receive a higher loan quantity with an ARM (due to the lower preliminary rate of interest). Yearly ARMs have actually historically outperformed set rate loans.

Rates may increase after the change duration. If you don't believe you'll save enough upfront to offset the future rate boost, or if you don't wish to risk having to re-finance, reconsider. What should I search for? Look thoroughly at the frequency of modifications. You'll get a lower beginning rate with more regular adjustments but likewise more unpredictability.

Which Australian Banks Lend To Expats For Mortgages Fundamentals Explained

Counting on a refinance to bail you out is a huge threat. Here are the types of ARMs provided: Your rates of interest is set for 3 years then changes yearly for 27 years. Your rate of interest is set for 5 years then adjusts annually for 25 years. Your rates of interest is set for 7 years then changes every year for 23 years.

You'll also wish to consider whether you desire or receive a government-backed loan. Any loan that's not backed by the government is called a conventional loan. Here's a look at the loan types backed by the government. FHA loans are mortgages guaranteed by the Federal Housing Administration. These loans are designed for customers who can't create a big deposit or have less-than-perfect credit, that makes it a popular option for novice house purchasers.

A credit rating as low as 500 may be accepted with 10 percent down. You can look for FHA loans on Zillow. Since of the fees related to FHA loans, you might be much better off with a traditional loan, if you can receive it. The FHA requires an upfront mortgage insurance coverage premium (MIP) as well as http://devintnfh820.raidersfanteamshop.com/what-does-what-are-the-main-types-of-mortgages-mean a yearly mortgage insurance coverage premium paid monthly.

Conventional loans, on the other hand, do not have the in advance fee, Go here and the personal home loan insurance (PMI) required for loans with less than 20 percent down instantly falls off the loan when your loan-to-value reaches 78 percent. This is a zero-down loan provided to qualifying veterans, active military and military families.

Unknown Facts About How Many New Mortgages Can I Open

For one, unlike many loans, you don't need to make any monthly payments. The loan can be used for anything, whether that's debt, health care, everyday expenditures, or purchasing a getaway home. How you get the money is likewise flexible: You can select whether to get a swelling amount, month-to-month dispensation, credit line, or some combination of the 3.

If the house is sold for less than the quantity owed on the home mortgage, Debtors might not need to repay more than 95% of the home's appraised value because the home mortgage insurance coverage paid on the loan covers the rest. You can likewise use a reverse mortgage to acquire a main home if you have enough funds for the down payment (you basically need to pay about half of the house's cost utilizing your own money and cost savings), in addition to the capability to pay for other home costs, such as residential or commercial property taxes and insurance.

If you vacate your house, the loan can likewise become due. Reverse mortgage interest rates can be fairly high compared to traditional home loans. The included expense of home mortgage insurance does use, and like many home loan, there are origination and third-party charges you will be accountable for paying as explained above.

If you decide to take out a reverse home mortgage, you might wish to talk with a tax consultant. In general, these earnings are ruled out taxable income, but it might make sense to find out what holds true for your particular circumstance. A reverse home mortgage will not have an effect on any routine social security or medicare benefits.

Not known Factual Statements About How Mortgages Work For Dummies

Depending on your monetary requirements and goals, a reverse mortgage might not be the very best choice for you. There are other ways to tap into cash that could offer lower costs and do not have the exact same rigid requirements in regards to age, home worth, and share of mortgage paid back such as a home equity line of credit or other loan options.

An individual loan might be a good choice if you need to pay off high-interest financial obligation, fund home restorations, or make a big-ticket purchase. A personal loan may be a good choice if you require to pay off high-interest debt, fund home remodellings, or make a big-ticket purchase. SoFi offers personal loans ranging from $5,000 to $100,000, and unlike with a reverse home mortgage, there are no origination costs or other covert expenses.